Dave Van Knapp of SensibleStocks.com publishes an annual overview of the dividend-paying stock scene. This year’s edition came out last month. Dave was kind enough to send me a copy of The Top 40 Dividend Stocks For 2010, and I’ve read through all 145 pages of it.

To the point: this is the best dividend-stock book I know. If you’re interested in building a portfolio of dividend-paying stocks, start with this book. Below, I’ll share some excerpts from the book to show what you can expect to learn, and put to use right away.

Here’s the table of contents:

- Introduction

- A Look Back at 2009 and Forward to 2010

- What Are Dividends?

- Why Invest in Dividend Stocks?

- What Are the Characteristics of the Best Dividend Stocks?

- Creating and Managing Your Dividend Stock Portfolio

- The Top 40 Dividend Stocks for 2010

- Easy-Rate Scoresheets for the Top 40

- Disclaimer and Important Information

From the introduction:

There are two phases to the [sensible dividend investing] process. The first is to identify the “best” dividend-paying companies. Ones that:

- Are financially solid

- Have a good initial yield at the time of purchase

- Consistently raise their dividends

- Are available at decent valuations

- Are relatively low in risk as to both their dividends and stock prices (recognizing that stock market risk can never be fully eliminated)

The second phase is portfolio management. The approach presented in this book emphasizes making timely decisions to buy, sell, hold, or replace stocks; maximizing dividend yields and dividend increases; sidestepping dividend cuts; and avoiding outright loss of capital wherever possible.

From Chapter 2:

Overall dividends paid by S&P; 500 companies declined by 21% in 2009. Early in the year, monthly records were repeatedly set for annual percentage declines in total dividends paid and the sheer number of decreases announced. As you might expect, financial companies were hit particularly hard. They plunged from accounting for 30% of all dividends at their peak to only 9% by the end of 2009. . . .

[However,] 35 of [last year’s] Top 40 stocks (88%) increased their dividends in 2009. The median increase was 5.5% and the average increase was 4%, compared to the 21% loss in dividends paid by the S&P; 500’s stocks.

For 2010, Dave agrees with Standard & Poor’s, which expects an overall 5.6% increase in dividends in 2010.

In Chapter 4, he presents the case for dividend stocks:

Simply stated, the case for dividend stocks goes like this:

- Dividends are always positive.

- The best dividend-paying companies raise their dividends regularly, usually at a pace that exceeds inflation.

- Dividends are not just for current income. Dividends can be re-invested to build wealth.

- Re-invested dividends compound, accelerating the wealth-building process.

- Dividend stocks offer (with some risk) the potential for price appreciation in addition to the dividends they pay.

That’s it. Five bullet points. Many investors consider dividend investing to be boring. Personally, I find the prospect of building a “cash machine” of ever-increasing dividend-paying stocks to be rather exciting. . . .

Studies show that dividends have accounted for half or more of the total return of the stock market over very long terms. This may be surprising considering how little publicity dividends get. There is no widely followed dividend index that gets the kind of publicity given every day to the Dow, the S&P; 500, and the NASDAQ — all of which reflect price changes only, and therefore give only half the picture of “how stocks are doing.”

Also in that chapter, Dave provides a simple explanation of how, unlike bonds, dividend payouts can rise over time so that your yield increases, one of the best benefits of a reliable dividend-paying stock:

If you own shares in a dividend-paying company that increases its dividends — meaning that the per-share payout goes up, as shown in the illustration — something very attractive takes place: Your yield on cost as a shareholder goes up.

Many dividend-paying companies have a long history of increasing their dividend regularly. Often this is done in line with their earnings growth each year. So a company with annual earnings growth of, say, 10% may increase its dividends 10% that year too. For comparison, in your job, how often do you get a 10% raise?

When a company increases its dividend, your yield on cost (that is, the yield on your original investment) goes up. This happens even though the current yield quoted in the newspaper stays the same.

How can this be? It’s simple math.

Say you purchase stock in Dividend Inc. when its price is $100 per share and its current yield is 3%. So you buy $1000 worth (10 shares) and the stock pays you $30 that year.

No matter how the stock’s price changes over the coming years, your personal yield (= yield on cost = yield on your original investment) will always be based on that $1000 that you invested in the stock.

Let’s say that Dividend Inc.’s longstanding practice is to increase its dividend in line with earnings. If it increases its earnings 10% per year, that means in Year 2 the company pays out 10% more to you, or $33, so the yield on your original $1000 investment increases to 3.3%.

Note that it no longer matters what Dividend Inc.’s current yield is. If the stock’s price rises exactly in line with the company’s increased earnings (which would happen in a rational market), Dividend Inc.’s price next year is also 10% higher ($110 per share), so the newspaper will still list the current yield as 3% ($33/$110). But that only applies to new buyers, not you.

To improve how effectively his Easy-Rate scoring system identifies top dividend-paying stocks on the market, Dave tweaks it each year to place more emphasis on higher-yielding stocks without adding much additional risk. This year was no exception.

The system uses data from DRiPInvesting.org, Morningstar.com, StandardandPoors.com, and others to find the companies with the best business models; healthy finances; strong earnings, low debt, and other solid fundamentals; a decent analyst backdrop; yield higher than 3.0% with a three-year total percentage dividend increase of at least 16%; a history of raising the dividend; and a reasonable stock valuation. The sweet spot contains companies with a high enough yield to be worthwhile, and a growth rate of that yield that is sustainable.

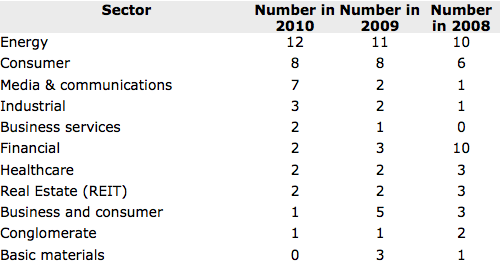

That rather lengthy, thorough process winnowed out the following sector breakdown in this year’s top 40 stocks, as compared with the two prior years:

The book presents this year’s top 40 in four tables, each with a different sort parameter: alphabetically, by company quality score, by total score (company quality + valuation), and by current yield percentage. The top five dividend yields are:

9.8%

8.4%

8.2%

7.6%

7.3%

Each of the 40 stocks is presented on a completed Easy-Rate score sheet, showing exactly why it made the cut. The completed score sheets are also useful as examples of the kind of research you need to do on companies outside the compact list of 40, if you’d like to apply Dave’s methods to your own dividend-paying candidates.

Finally, Dave discusses what to do with stocks purchased from 2

009’s list that did not make this year’s list. In most cases, but not all, he suggests keeping them.

It’s another winning edition of this annual survey. Dave sells it in PDF form for $39 here.