Last week saw a subtle but important shift in the way economic data were interpreted. During most of the rally, any improvement in data was heralded as proof that the worst was behind us and the future a ramp upwards with only the degree of incline in question. Merely an upward bias in economic data was enough to give stocks an upward bias as well. Last week, however, more attention was paid to the strength of the data instead of its direction alone. Finally, the market may be asking if the recovery is good enough to justify high stock prices. Over the past two weeks the answer has been, “No.”

What could follow on the heels of such a shift is a further backing up from debating the incline of recovery to questioning whether an upward bias is guaranteed after all. With loan defaults rising, jobs about as common as sense in Congress, and central banks eager to pare back stimulus, more people appear to be wondering if another leg down is inevitable.

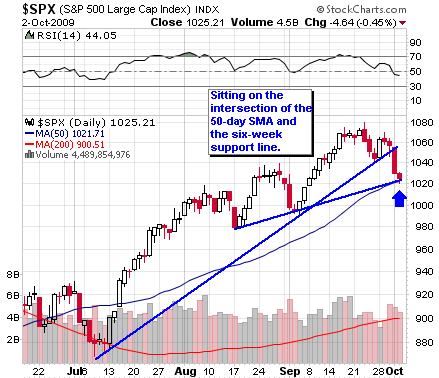

Let’s look at the technical picture for the main stock indexes of the world’s four financial centers: the S&P; 500 in New York, the Nikkei 225 in Tokyo, the SSE Composite in Shanghai, and the FTSE 100 in London.

Here’s New York:

Here’s Tokyo:

Here’s Shanghai:

Here’s London: