Today’s reading is a collection of excerpts suggesting caution.

Doug Kass:

Despite the strong share price momentum and the aforementioned emerging optimistic economic/profit consensus, I continue to hold on to the variant view that the markets have likely peaked for the year based on the existence of nontraditional headwinds, an end to decades of aggressive credit expansion and financial inventiveness, a still-vulnerable housing recovery (in the form of outsized phantom inventory challenges) and a still-fragile consumer — among other factors.

Full article here.

Ambrose Evans-Pritchard:

If you look at the sheer scale of global stimulus this year, what shocks is how little has been achieved. China’s exports were down 23pc in August; Japan’s were down 36pc; industrial production has dropped by 23pc in Japan, 18pc in Italy, 17pc in Germany, 13pc in France and Russia and 11pc in the US. Call this a “V-shaped” recovery if you want. Markets are pricing in economic growth that is not occurring.

Full article here.

Financial Times:

Banks round the world have still to reveal about half of their likely losses resulting from the financial and economic crisis, the International Monetary Fund said on Wednesday, warning that there was still a “significant” risk of another downward lurch in the global recession.

The IMF described credit risks as remaining “elevated” even though financial conditions have improved significantly since spring.

It said these risks, alongside weakened banks, were likely to depress the availability of new credit and damp the global economic recovery unless significant additional capital was raised to improve the health and lending capability of banking systems.

Full article here.

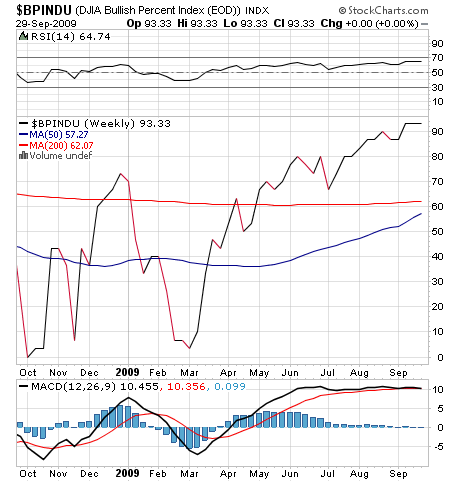

Finally, check out the bullish percent index for the Dow: