The hopeless romantic in me fell for Starbucks. Who could resist the topless logo lady kept barely modest by flowing tresses alone? She proved to be my siren on the foggy rocks. My ship, the JSS Portfolio ran aground to the sound of her charms.

Which is to say I was early on Starbucks.

I’ll save you the trouble of joining the email chorus mocking me on this one, by coming clean. Wrong more than I should be? Yes. Dishonest? No.

I started liking Starbucks way back in January. Chuck Jaffe invited me onto his Your Money Radio program that month and I told his listeners that it was amazing to see the world’s largest coffee retailer on sale for less than $20 per share. “That’s down to almost half what it was a year ago,” I gushed. “This is not some flier, either. Folks, this is Starbucks I’m talking about!”

It’s still Starbucks I’m talking about, but that under-$20 bargain is now an $8 bargain, and still falling. The legion of investors hating the stock has multiplied, and they all know how to reach me. Among the more polite notes I received recently was this one from a professor who recently subscribed to The Kelly Letter:

They have no chance in Europe at all, and they have too many outlets in the U.S. Perhaps Asia might be the place for them, but if then in a small way. When I was in mainland China in 1980 as a guest of the Chinese Academy of Sciences, it was impossible to get a good cup of coffee in Beijing. The same problem existed in Shanghai. Thus, for foreigners, a good cup of coffee in China would probably be profitable.

However, in Europe (excepting, perhaps, England) they have no chance. In Vienna there are a few Starbucks, but only frequented by foreigners. It is absurd to go to Starbucks in Vienna when one can go to Sacher or Demel, established in the time of the Austrian Emperors.

Good points, but I don’t think Starbucks ever intended to brew a better cup of coffee than places serving Austrian royalty. As with McDonald’s, Starbucks aims for the fat part of the bell curve where a good enough cup of coffee meets a fair enough price in an atmosphere that’s pleasant enough and — importantly — convenient.

Here in Japan, Starbucks is a sensation and I suppose that’s part of why I watched it all the way down to my first buy at $18 and thought I was pulling a fast one to grab a piece of the global empire at that price. I kept buying during the year. My cost basis is $13 now. It’s going to take a 63% gain just to get me back to break-even.

Yet, every time I walk into a Starbucks and smell the coffee and hear the voices of the Japanese workers welcoming customers, I’m proud to be an owner. I may not be as twitterpated with Greenie anymore, but I’m confident she’ll rush back to my arms one day with a 63% smile on her face.

Here’s why.

It almost goes without saying that the stock is a bargain, but only almost so let me say a little about it. At eight and change, SBUX has a PEG ratio of only 0.5. That’s less than half the S&P; 500’s PEG of 1.1, and you may have noticed that the S&P; itself has come down a tad this year. Even by P/E alone, SBUX trumps the index with a 9 versus the 500’s 11.

Along with everybody else in this dreamy economy, Starbucks’ business results have suffered. Even when we factor in the slowdown, however, the company isn’t anything like the charred trees of the subprime forest fire the government is trying to douse with soggy taxpayer money. Its 2007 year-on-year revenue growth was 20.9%. Now it’s 10.3%. A lot slower, sure, but not exactly hopeless.

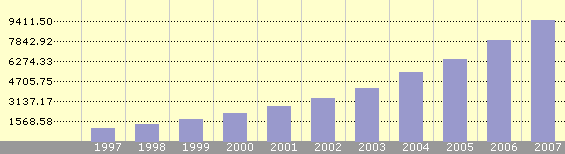

In fact, I’d say the 10-year revenue chart is a thing of beauty, consistent with this little fling of mine. Courtesy of Morningstar, look at her shine:

You’d never guess that’s a company caught in the teeth of recession, now, would you? I know I’m showing you how she looks all dressed up for the prom, when the market’s seeing her as she looks first thing in the morning, better known as a price chart. We’ll skip that, though, because she’s a lady and you’re too polite to ask and I’m too gracious to offer.

One thing to bear in mind is that on top of the recession headwind, Starbucks is in the middle of a restructuring that includes closing slow stores; reducing headcount; and re-invigorating the Starbucks experience with new equipment, better training for workers, and an expanded menu. Restructurings are always hard on a business. Restructuring while credit markets dry up and talk of a 100-year bear market circulates, is even harder. That’s especially true of Starbucks, which depends on consumer confidence and discretionary cash, both at low levels.

As the recession grinds on, will consumers drink even less coffee? That’s the great fear, of course. Even if they don’t drink less coffee overall, they may elect to get their java at a more affordable location. Usually McDonald’s is cited here as the cheaper alternative, but I was thinking more of our own kitchens. I make a pretty mean cup of coffee for a few pennies, and I’m sure others can, too.

I don’t know about you, but the taste of the coffee is not the only reason I go out for a cup. I want to get out. I want to sit on a couch and read something and nibble on something and hear the sound of machines working and the people mingling and the whole scene. That’s what I’m paying for. Should we all get dirt poor and start cutting way back, I think I might just save a few shekels for the much needed escape from recessionary life. We could all feel poor together at Starbucks.

That’s anecdotal, though, and I admit that a poorer consumer is not in Starbucks’ best interest.

One thing that is in Starbucks’ best interest is how much people love coffee, and how much growth opportunity that creates for the company. A common objection to Starbucks is that it has too many stores. The market is saturated, say the naysayers, who are everybody except me and CEO Howard Schultz. It isn’t saturated, though. Even with its runaway success over the years, Starbucks commands only a 10% share of the U.S. coffee market. Overseas, its market share is around 1%. If 90% and 99% share being up for grabs isn’t growth potential, douse me with espresso.

Now, when it comes to ready-to-drink coffee, it’s a different story. Thanks to a smart partnership with PepsiCo, which knows a thing or two about getting drinks into people, Starbucks commands 85% of that market. There’s not much left to take, but that’s because the company took the market already and now enjoys a stream of cash from all that can coffee warming hands in winter.

Are there challenges? Of course, hence the current share price. I would say the encroachment of McDonald’s and Dunkin’ Donuts on Starbucks’ turf is the main problem. I mean, the mere existence of DunkinBeatStarbucks.com is a bad sign. There’s more competition; that leads to lower margins.

So be it.

When I run the reduced cash flow expectations from the latest quarterly report and factor in cost savings from

restructuring, Starbucks doesn’t look as promising as it did in January when I first sang its praises. However, I still come up with a reasonable value at $20. With a P/E expansion that should happen when the economy and stock market recover, I can paint a convincing picture for $30 per share.

Even from my bewitched cost basis of $13, that ain’t bad. From today’s $8, it’s positively enchanting.

As this star-crossed lover pulls the petals from a flower reciting “she loves me, she loves me not,” I count ahead to the end of the circle and see how the pattern ends: she loves me.

Now give me a 63% gain, lady!